5 Takeaways on the 529 Savings Plan Landscape

Since their launch more than 20 years ago, 529 education savings plans have helped students and their families better access higher education through tax-advantaged investing. Moreover, 529 plans have become relevant to an increasing number of investors as their use cases have expanded over the years (the most recent evolution including Roth IRA rollovers).

In this annual review of 529 plan trends, we track key metrics investors should keep an eye on, including assets, fees, and more.

Takeaways on the 529 Savings Plan Landscape

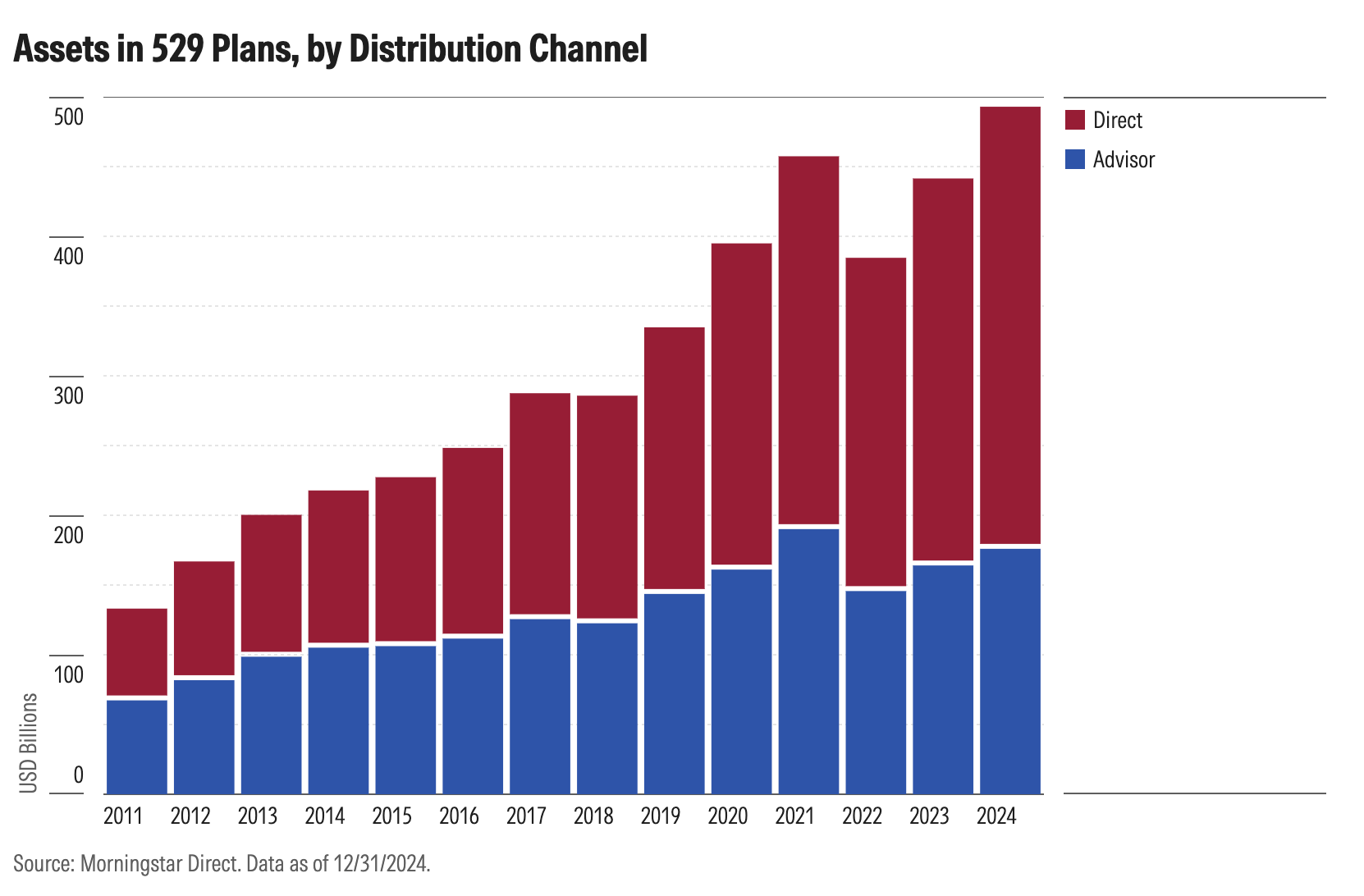

- 529 industry assets reached a new all-time high of $492.9 billion in 2024, up 11.6% from 2023, thanks to continued investor interest and a soaring stock market.

- Industry concentration remains high: Vanguard, Capital Group, and TIAA-CREF now manage over half of total assets, with TIAA-CREF overtaking Fidelity in 2024.

- Plans are becoming more straightforward: Over 80% of plans offer a single glide path, though some continue to provide expanded choice for investors.

- Progressive glide paths now account for 43% of plans. While some still appear steep, they generally offer smoother derisking than traditional stepwise designs.

- Direct-sold plans continue to be cheaper investment options than advisor-sold ones, with an average fee of 0.31%.

529 Industry Assets Set a Record

Investors’ assets in 529 plans reached a record high of $493 billion in 2024, an 11.6% increase over 2023’s $442 billion. Participants benefited from a strong stock market rally and higher interest rates that benefited cash and equivalents, which tend to play a key role in portfolios near and through college enrollment. The expanded use cases, such as K-12 education, student loan repayment, and apprenticeships, also likely attracted more savers to the plans.

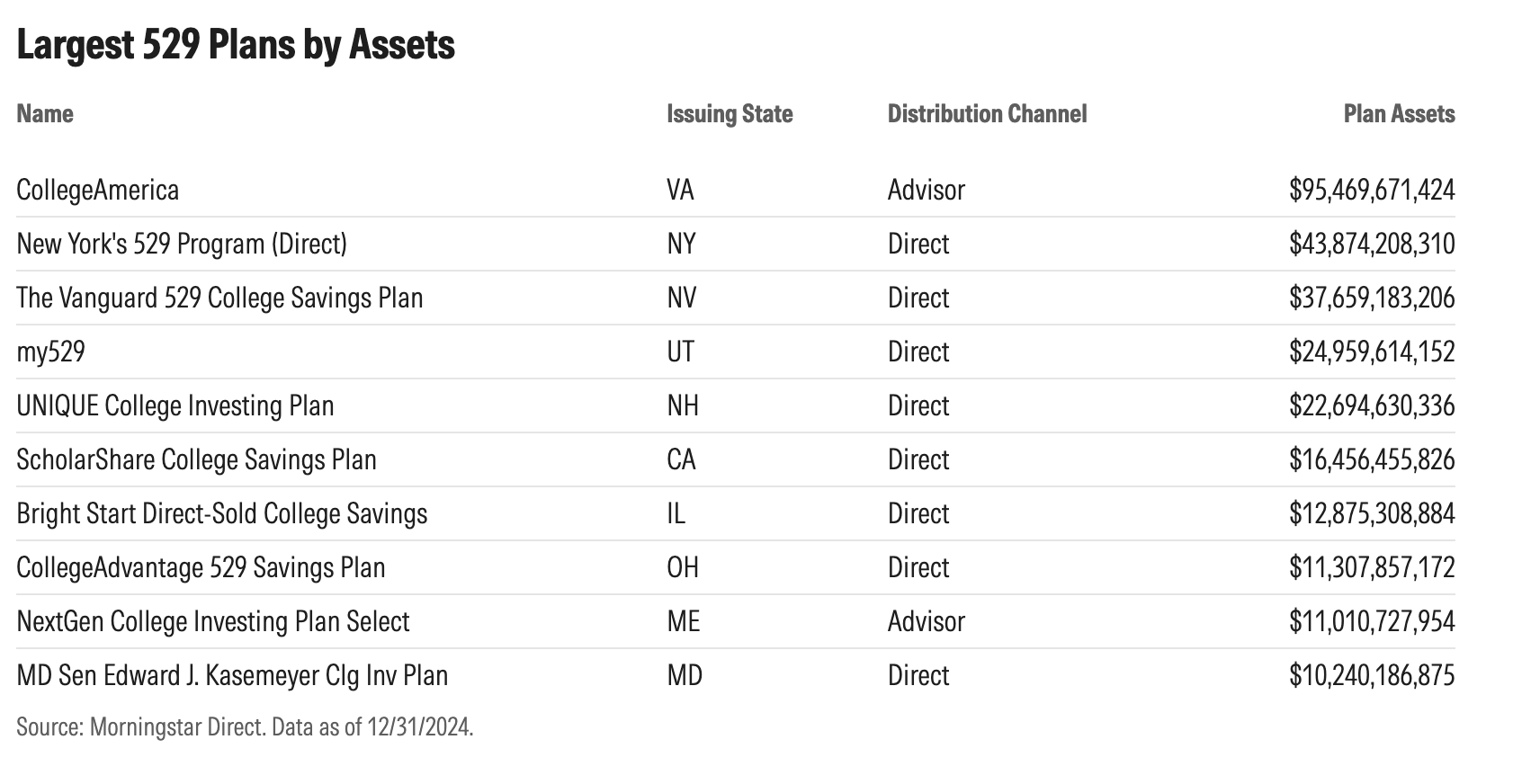

Investors Continue to Prefer Direct-Sold Plans, With One Big Exception

Most 529 investors continue to use plans sold directly to individuals rather than through a financial advisor. Roughly 64% of 529 plan assets were in direct-sold plans at the end of 2024, up from 43% 10 years ago. Direct-sold plans are available to do-it-yourself investors and those who do not have access to a financial advisor. They also tend to be cheaper than advisor-sold plans, effectively increasing the chance of meeting one’s savings targets.

One exception to this rule is CollegeAmerica, an advisor-sold plan offered by Virginia and managed by Capital Group. Capital Group’s high-quality funds, strong reputation, and distribution capabilities helped the plan exceed $95 billion in assets, the largest among all 529 plans and more than double that of its runner-up, New York’s 529 Program

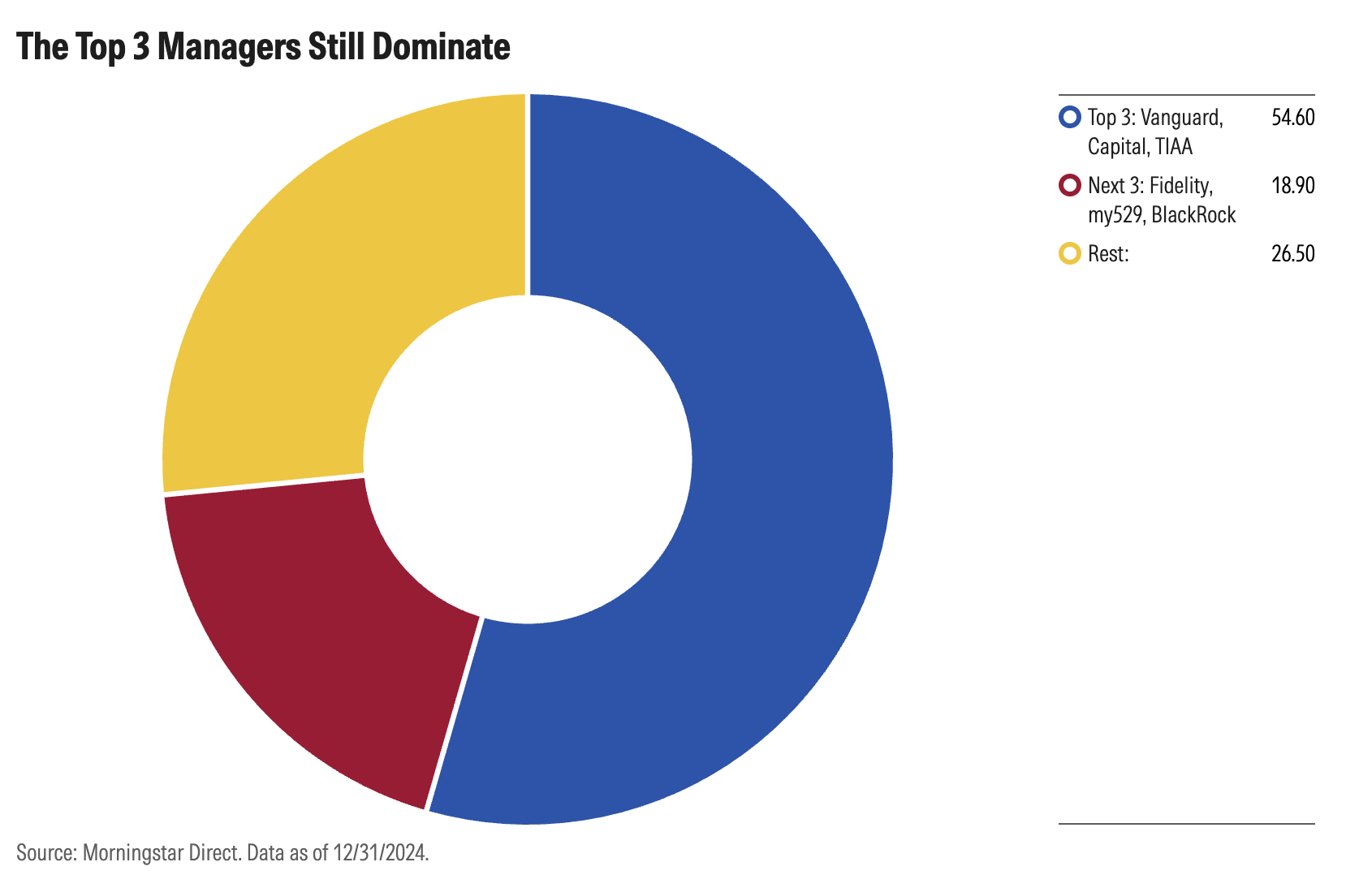

Vanguard Continues to Be the Most Popular 529 Plan Provider, Fidelity Falls Out of the Top Three

Although Capital Group manages the largest plan, it’s the low-cost champion, Vanguard, that is the most popular option for 529 plans. Both Vanguard and Capital Group have remained the top two managers of investors’ college savings, thanks to their broadly attractive mutual fund lineups and modest-to-low fees.

However, the third-largest 529 plan manager is now TIAA-CREF, which surpassed longtime top-three manager Fidelity over the past three years. The firm has taken over substantial plans in recent years, including Illinois’ direct-sold Bright Start 529 plan, as states have found the firm’s dedicated 529 team and focus on lower costs appealing.

These top three managers control more than half of all 529 plan assets, though the industry looks slightly less top-heavy now. Three years ago, the three largest providers garnered 60% of assets. That number has since declined to roughly 55%.

The Top 3 Managers Still Dominate

The largest 529 managers after the three leaders are Fidelity, my529 (which runs only a large Utah 529 plan), BlackRock, Wilshire, and recordkeeper Ascensus.

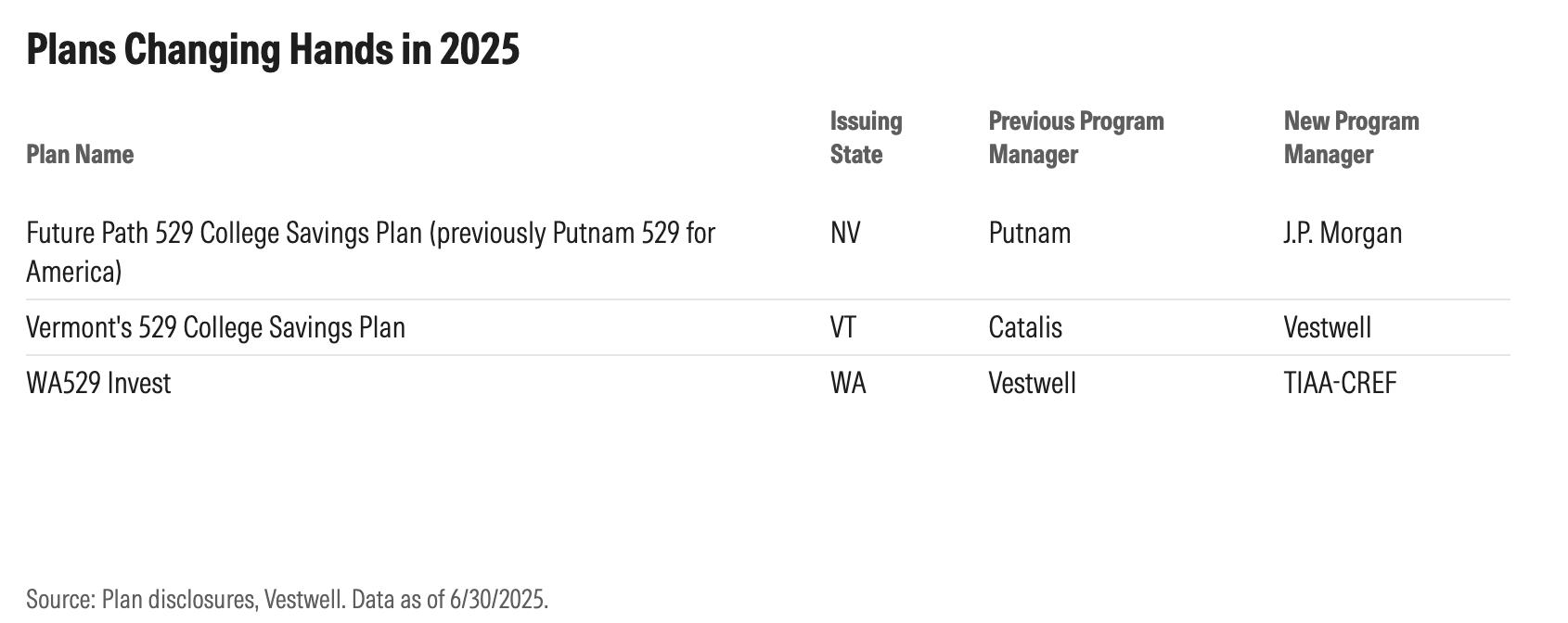

529 plans haven’t done much hiring and firing of asset managers in recent years. Illinois Bright Start was the only one to do so in 2024. And there were no changes on the investment side in 2023. 2025 looks to be more active: TIAA-CREF took over Washington’s plan from Vestwell, JPMorgan Chase now runs a Nevada plan previously managed by Putnam, and Vestwell is expected to take over a Vermont plan later this year. TIAA-CREF is also expected to take over Kansas’ plan from American Century in 2026.

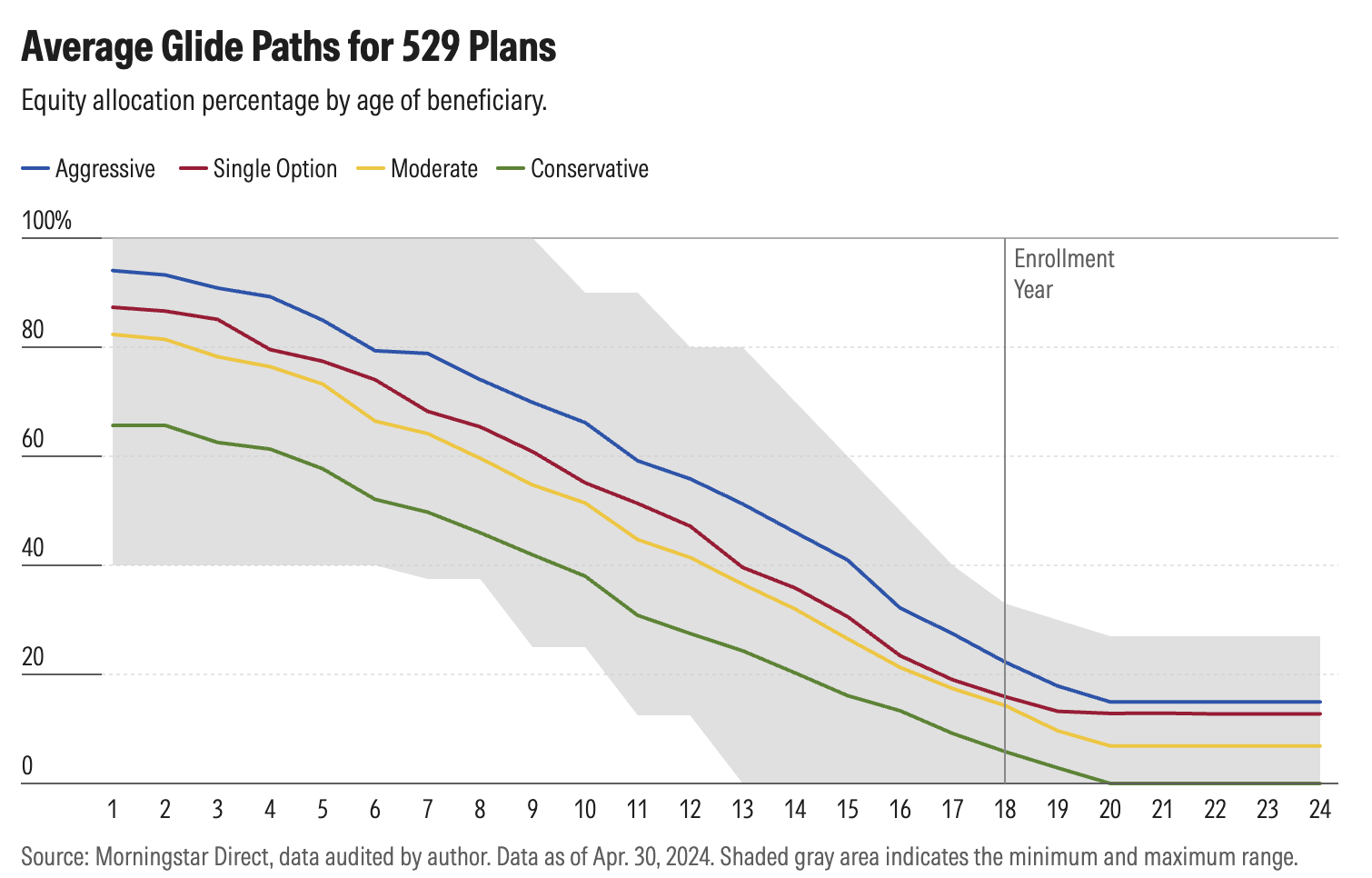

Most 529 Plans Do the Thinking and Choosing for Investors

Many 529 account holders are hands-off investors who utilize age-based or target-enrollment portfolios. These portfolios start with a large allocation in risky assets (generally stocks) when the beneficiary is young. As the beneficiary grows older, they transition to a more conservative portfolio by allocating more to bonds and cash or cash equivalents, like stable value funds. A glide path determines how the allocation shifts to a more conservative positioning as the beneficiary grows closer to college enrollment.

One of the more meaningful developments throughout the past several years has been the continued adoption of progressive glide path structures, in which asset allocations adjust gradually within a given enrollment-year portfolio. As this approach becomes more common, we have combined our analysis of single-path and progressive-path plans for a more holistic view.

A clear majority of plans—more than 80%—offer just one glide path, reinforcing the idea that plan sponsors and investment managers are consolidating around a default recommendation. On average, these start at roughly 91% equity exposure in early years and taper down to around 16% equity exposure by the time the beneficiary turns 18. It falls somewhere between the average “moderate” and “aggressive” glide paths offered by plans that support multiple glide paths.

This trend is in part enabled by the popularity of enrollment-year portfolios. With investors selecting a portfolio aligned with a specific date, there’s less need to segment by individual risk tolerance. If an investor deems themselves more aggressive or conservative than an average investor, they can simply shift their enrollment year. That said, some plans continue to offer multiple glide paths to accommodate varying preferences. As of this review, about 13 plans offer more than one track based on risk tolerance.

Morningstar does not take a prescriptive view on whether plans should offer a single glide path or multiple tracks. Providing investors with choice—whether by risk tolerance, investment style, or values—can be valuable, particularly for those with clear preferences or more comfort navigating portfolio decisions. At the same time, a single, well-constructed glide path can mitigate decision fatigue and guide less confident investors toward an age-appropriate allocation. Ultimately, the right approach depends on a plan’s goals and investor base.

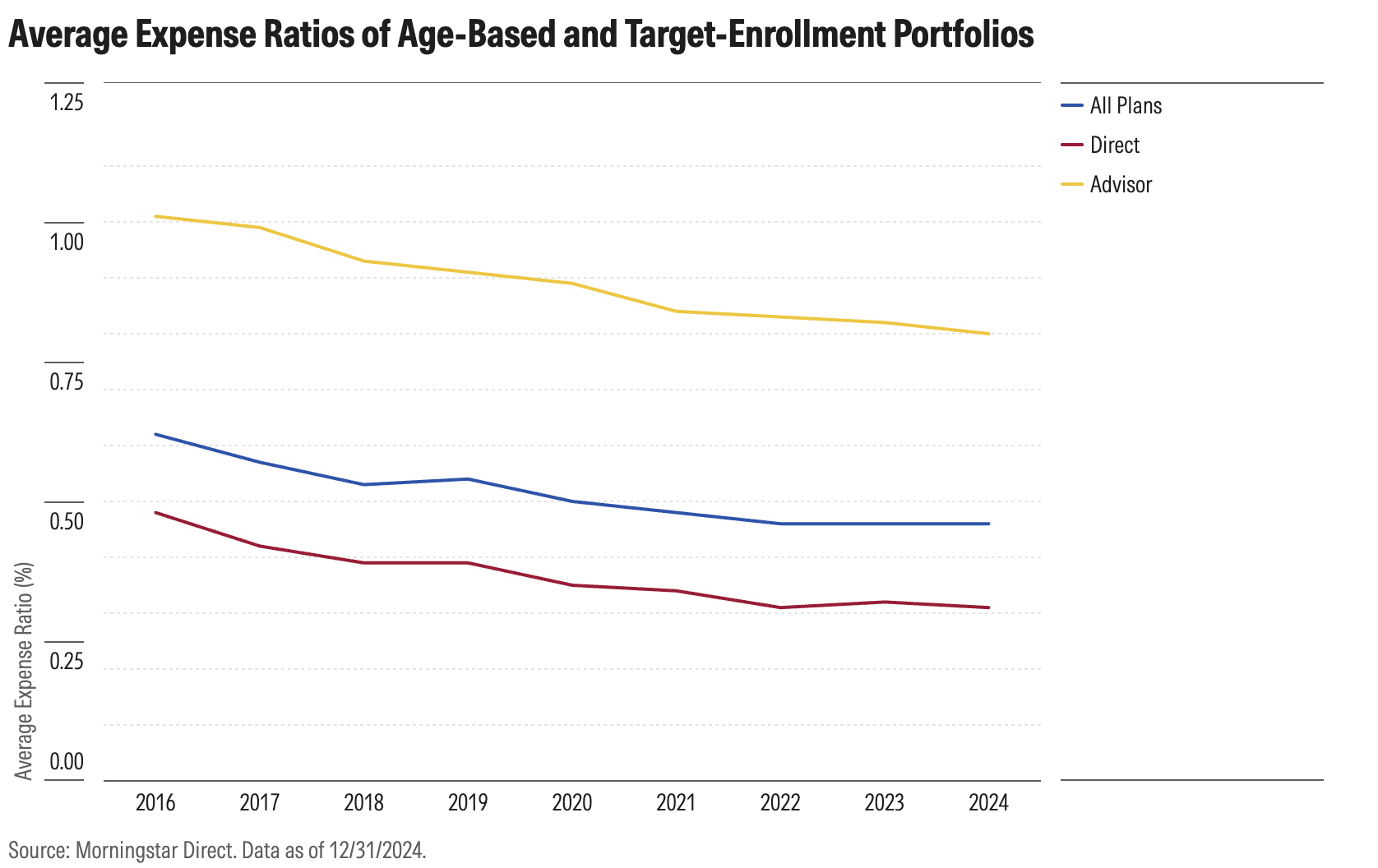

529 Plans Remain a Great Deal for Investors

529 plans have meaningfully reduced their fees over the past several years, making it much cheaper to save for education in a tax-deferred way. Although the fee compression has slowed somewhat in 2024, 529 plans’ overall affordability remains a win to be celebrated.

Average fees for age‑based and target‑enrollment 529 portfolios held steady at 0.46% in 2024. Advisor‑sold plans extended their multiyear cost slide to a record‑low 0.80%, while direct‑sold plans were unchanged at 0.31%. The pause in fee compression at the cheaper end suggests the industry’s decade‑long shift to lower‑cost, largely passive funds has captured most of the easy savings, leaving limited room for further cuts. Even so, direct‑sold options still boast a sizable edge—nearly 50 basis points cheaper than their advisor‑sold counterparts.

Source: https://www.morningstar.com/personal-finance/5-takeaways-529-savings-plan-landscape-2